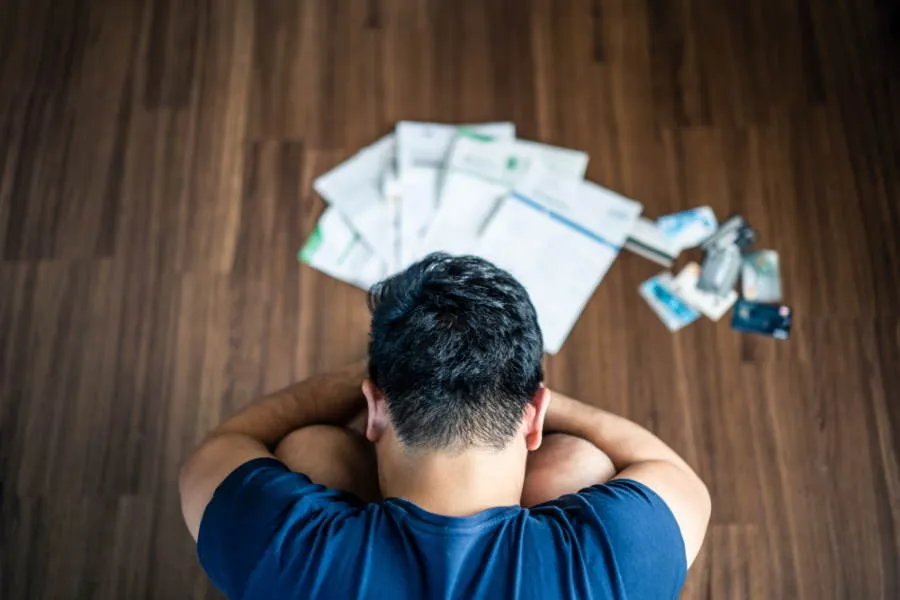

If your money is constantly running out before the end of the month and you find yourself constantly in an overdraft, you may be in problem debt. But don’t worry there is help available and Angel Advance can provide you with free debt advice to understand your options.

What is problem debt?

Problem debt, or over-indebtedness, is a term that refers to someone who is unable to pay their household bills or debts. Anyone can find themselves in problem debt due to a significant change in their circumstances – such as losing a job or splitting from a partner – or it can occur when credit responsibilities have been overestimated by budgeting incorrectly.

The last report issued by the Money Advice Service on problem debt – published in September 2018 – indicates that 17.2% of adults in the UK are over-indebted; that’s almost 9 million people. Whilst the over-indebted population is reported to be younger, more likely to rent, and more likely to have children, it can affect anyone at any point in their lives.

So, why does it matter? Debt and mental health are intrinsically linked: half of UK adults that are in problem debt also live with a mental health illness and 25% of people with a mental health illness find themselves in debt. Your mental health is paramount, so recognising that you are over-indebted, or about to fall into problem debt, could be significant to avoid impacting your health and well-being.

Top 5 identifiers of problem debt

- Always in an overdraft – If you are one of the 26 million people in Britain who have an overdraft facility, and if you’re using that facility more than 8 out of 12 months, you could be in problem debt.

- Ignoring post or not looking at your bank statements – Not opening your post because you are concerned that it is an overdue bill could be an identifier of being in problem debt. If you don’t look at your bank statement for fear of how much you (don’t) have left over, or how far you may be in your overdraft, you might be over-indebted.

- Taking out credit to pay off credit – In other words, robbing Peter to pay Paul. Whilst this may seem like a short-term solution, it can result in your overall debt level increasing and interest rates becoming overwhelming.

- Hiding debt letters from your partner or family – If you have to hide letters about debt from your friends, family, or partner, it has clearly become a problem. If it wasn’t a problem, you wouldn’t have to hide it.

- Only making minimum payments to debts – It may be tempting to only make the minimum payment to your credit card, or it may be all that you can afford, but it will result in you paying much more than your original balance and you’ll pay back a significant amount in interest over time.

5 steps to freedom from ‘problem debt’

If you find that you have ticked one or more of the boxes above, you are more-than-likely having difficulty with your finances and it could lead to you falling into spiralling debt problems. But, there’s a way out.

Admit

The first step to tackling your debt problem, and usually the most difficult to overcome, is admitting that you are over-indebted. Once you concede, you can look for ways out of your problem debt.

Budget

Budgeting can be difficult and budgeting incorrectly may have been a factor in finding yourself in this position. Sit with a family member or friend and look through your income and spending – or look at our budgeting tips here – to see if you can cut back on non-essentials or reduce your variable spending to free up some vital spends.

Action

Cut up your credit cards to stop the temptation of using them as a safety net. We’d also recommend contacting your bank to see if they can waive any overdraft charges. 8.9 million people are potentially being charged overdraft fees that they don’t know or understand!

Save

22% of adults have less than £100 in savings leaving them susceptible to problem debt if any unexpected expenses crop up such as car maintenance or replacing broken household appliances. When budgeting, set aside a small pot for savings; it’ll build up month-by-month and should cover you for a rainy day.

Claim

When was the last time you checked what benefits you may be eligible for? The criteria for eligibility can change and so can your personal situation; use the online Benefit Calculator through Turn2Us here. Enter all your details as honestly as you can; it will confirm your entitlement and how to claim.

FINAL STEP – ADVICE

Overcoming problem debt could have a positive impact on your mental health, your relationships, and even your future job prospects. If you have followed our step-by-step guide and need one final lift out of the debt spiral, you may need to seek free debt advice, or even engage in a financial solution such as a debt management plan. To find out if a financial solution would benefit you and put an end to your over-indebtedness, use our free Online Debt Advice tool or contact us on 01925 599400.